![Checklist for Selling Your House This Spring [INFOGRAPHIC] Simplifying The Market](https://denverlivinghomes.com/wp-content/uploads/2023/02/Checklist-For-Selling-This-Spring-KCM-Share.png)

![Checklist for Selling Your House This Spring [INFOGRAPHIC] | Simplifying The Market](https://denverlivinghomes.com/wp-content/uploads/2023/02/Checklist-For-Selling-This-Spring-MEM.png)

A Smaller Home Could Be Your Best Option

Many people are reaching the point in their lives when they need to decide where they want to live when they retire. If you’re a homeowner approaching this stage, you have several options to explore. Jessica Lautz, Deputy Chief Economist and Vice President of Research at the National Association of Realtors (NAR), says: Read more

Spring into Action: Boost Your Home’s Curb Appeal with Expert Guidance

To sell your home this spring, it may need more preparation than it would have a year or two ago. Today’s housing market has a different feel. There are more homes for sale than there were at this time last year, but inventory is still historically low. So, if a house has been sitting on the market for a while, that’s a sign it may not be hitting the mark for potential buyers. But here’s the thing. Right now, homes that are updated and priced at market value are still selling fast. Read more

Finding Opportunities in the 2023 Denver Real Estate Market

Have you been sitting on the sidelines of the Real Estate market wondering if there will ever be a good point to hop in the game?

If so, then we have some good news for you. NOW is the time to explore opportunities in the current Real Estate market.

In this week’s video, we’re looking at how the recent decrease in buyer demand is creating a prime opportunity for someone interested in buying a home or an investment property.

With a more normalized market between buyers and sellers, we are seeing some homes sitting on the market a bit longer, buyers being able to keep contingencies in their offers, new home builders having ready-to-deliver inventory available, and buyers being able to get into neighborhoods that have been unattainable for the past few years.

Watch the video to hear more about all of the above AND MUCH MORE!

If you have given any thought to entering the housing market and are interested in having a home buying or selling consultation, contact us at the below link to connect!

![The Spring Housing Market Could Be a Sweet Spot for Sellers [INFOGRAPHIC] Simplifying The Market](https://denverlivinghomes.com/wp-content/uploads/2023/02/The-Spring-Housing-Market-Could-Be-A-Sweet-Spot-For-Sellers-KCM-Share.png)

![The Spring Housing Market Could Be a Sweet Spot for Sellers [INFOGRAPHIC] | Simplifying The Market](https://denverlivinghomes.com/wp-content/uploads/2023/02/The-Spring-Housing-Market-Could-Be-A-Sweet-Spot-For-Sellers-MEM.png)

Wondering What’s Going on with Home Prices?

The recent changes in home prices are top of mind for many as the housing market begins gearing up for spring. It can be hard to navigate misleading headlines and confusing data, so here’s what you should know about today’s home prices.

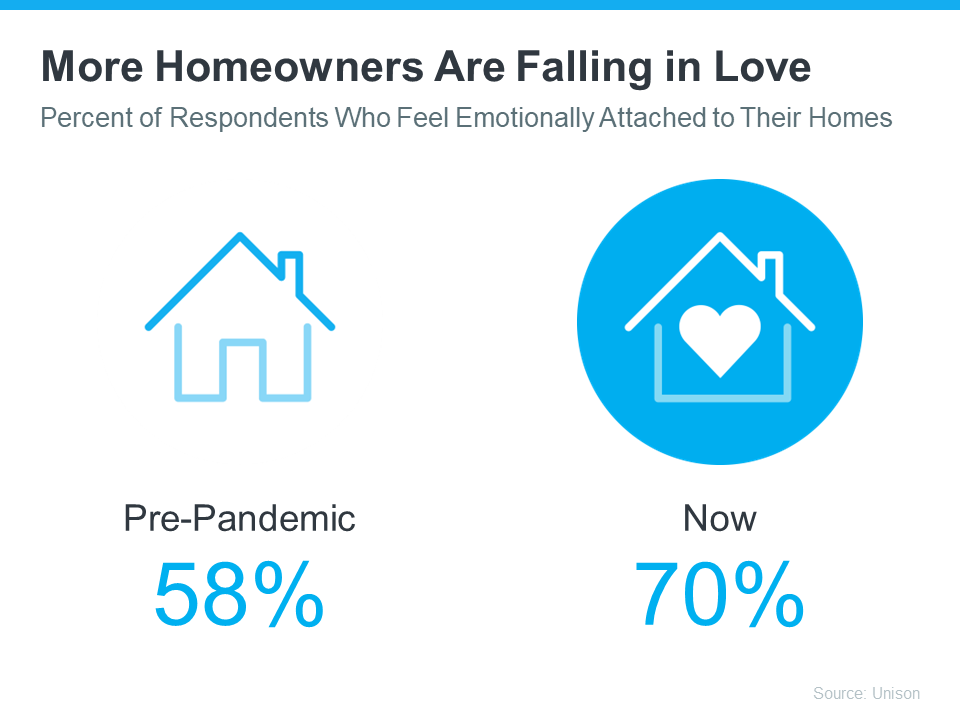

Why It’s Easy To Fall in Love with Homeownership

No matter how the housing market changes, there are some things about owning a home that never change—like the personal benefits it can provide. When you own your home, you likely feel a sense of attachment because of the comfort it gives and also because it’s a space that’s truly yours.

Over the last few years, we’ve fully embraced the meaning of our homes as we spent more time than ever in them. As a result, the emotional benefits our homes provide have become even more important to us.

As the most recent State of the American Homeowner from Unison puts it:

“. . . one thing has stayed the same: the home continues to be of the utmost importance and a place of security and comfort.”

The same study from Unison notes:

- 91% of homeowners say they feel secure, stable, or successful owning a home

- 64% of American homeowners say living through a pandemic has made their home more important to them than ever

It’s no surprise this study also reveals that homeowners now love their homes even more as our attachments to them have grown:

The National Association of Realtors (NAR) also explains:

“In addition to tangible financial benefits, homeownership brings substantial social benefits for [households], communities, and the country as a whole.”

In other words, not only does owning a home build your net worth over time, but it also gives you and your loved ones a place to thrive. And by living near people with shared experiences, homeownership helps you connect with your community and contribute meaningfully.

Bottom Line

Whether you’re thinking of buying your first home, moving up to your dream home, or downsizing to something that better fits your changing lifestyle, let me be the key to unlocking a home you can truly fall in love with.

Follow Us!