Why Now Could Be the Sweet Spot for Sellers

Over the past year, a lot of people put their moving plans on hold. Affordability weakened, and it was harder to find a home in budget, especially when inventory was so low. But things are shifting in a big way. Today, a rare balance is emerging — more choices when you buy, but still strong conditions when you sell.

If you stepped back from your plans last year, your trusted REMAX® agent wants you to know: the door is opening again. The only question is, will you walk through it before it closes?

Inventory Is Up — And That Changes the Game

Last year, the lack of options made it hard to make a move. There just wasn’t enough out there. And when something did pop up, it disappeared fast (or it wasn’t at your price point). And why sell your current home if it’s not clear if you can find another one you’d love?

This is why 70% of buyers decided to abandon their search last year.

But today, inventory is on the rise. Builders are building more homes. Sellers are listing their homes and re-entering the market. So, now you have choices that help you go from feeling stuck to maybe feeling ready to move again.

With more listings available and slightly more breathing room, many who paused before are starting to search again. And savvy sellers who act now can still capitalize on that pent-up demand.

The Real Sweet Spot

You might be wondering: if more homes are for sale now, does that mean it’ll be harder to sell your current home? Not quite.

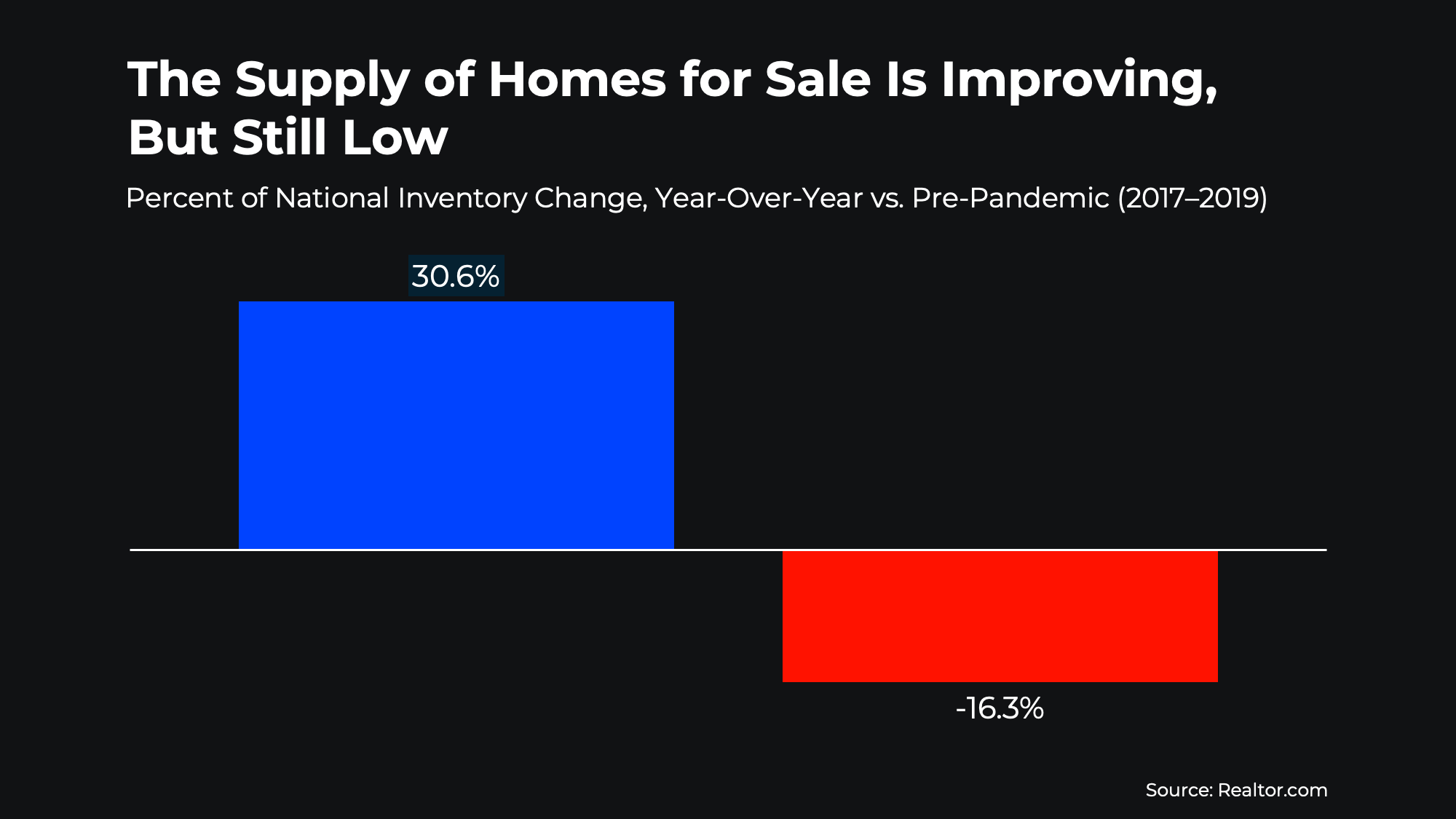

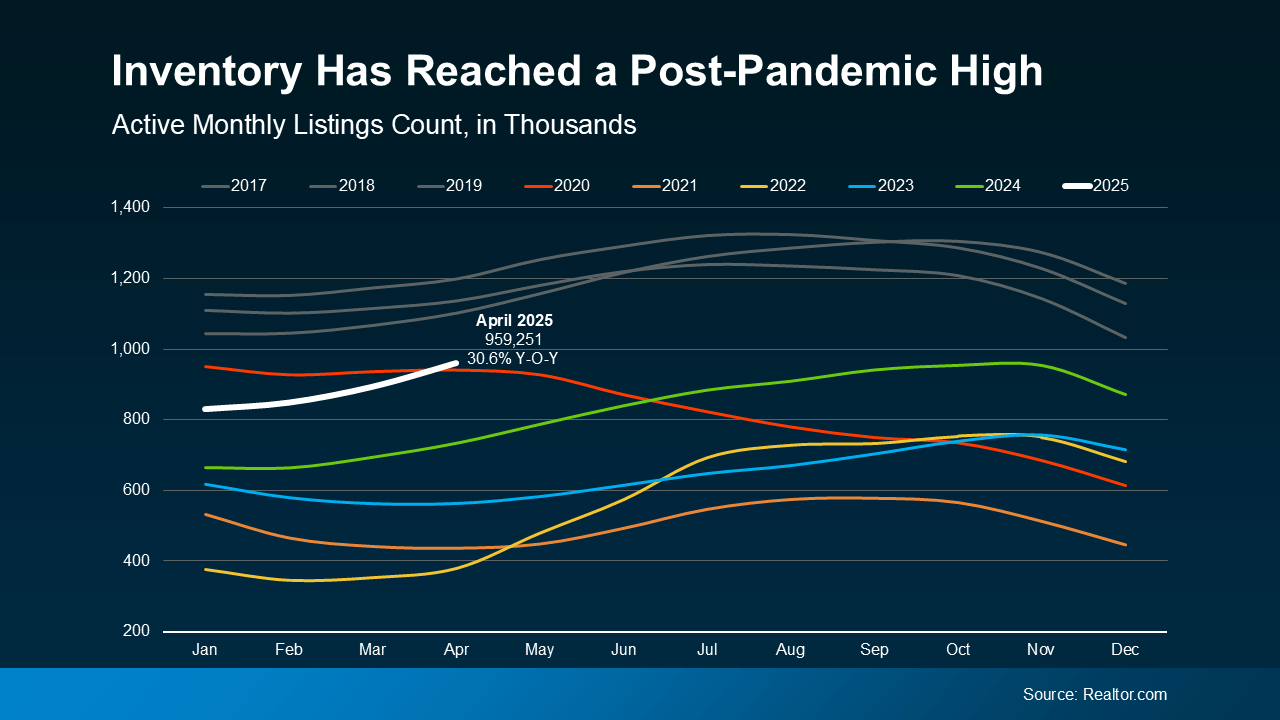

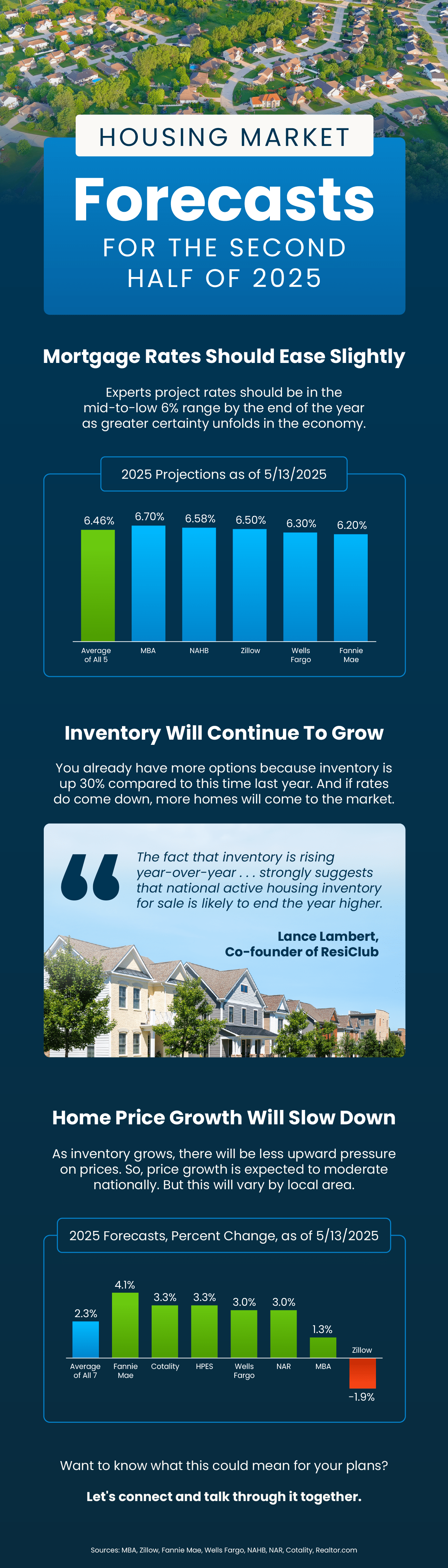

Data from Realtor.com shows inventory is up 30.6% compared to this time last year. But overall inventory levels are still about 16% lower than what’s considered a normal market (see graph below):

Basically, you’re not stuck anymore. But you’re not competing with a flood of listings either. That’s a seller sweet spot.

Basically, you’re not stuck anymore. But you’re not competing with a flood of listings either. That’s a seller sweet spot.

So, you have more homes to choose from when you move, but there still aren’t too many for sale.

That means your current home shouldn’t have any trouble attracting a lot of interest, especially if you lean on your REMAX agent to make sure it’s well-priced and well-prepped.

But this sweet spot may not last. Inventory has been climbing for over a year and a half now. And Lance Lambert, Co-Founder of ResiClub, says even more growth is coming:

“The fact that inventory is rising year-over-year . . . strongly suggests that national active housing inventory for sale is likely to end the year higher.”

Basically, if you wait too long, your home will be competing with your neighbors — and that could impact your ability to sell quickly and for top dollar. This is exactly the type of local insight only your REMAX agent can give you.

Bottom Line

This rare balance won’t last forever. The window is open, but it’s closing little by little as more listings hit the market.

Reach out to your trusted REMAX agent. That way, you can decide if this sweet spot in your area is the opportunity you’ve been waiting for.

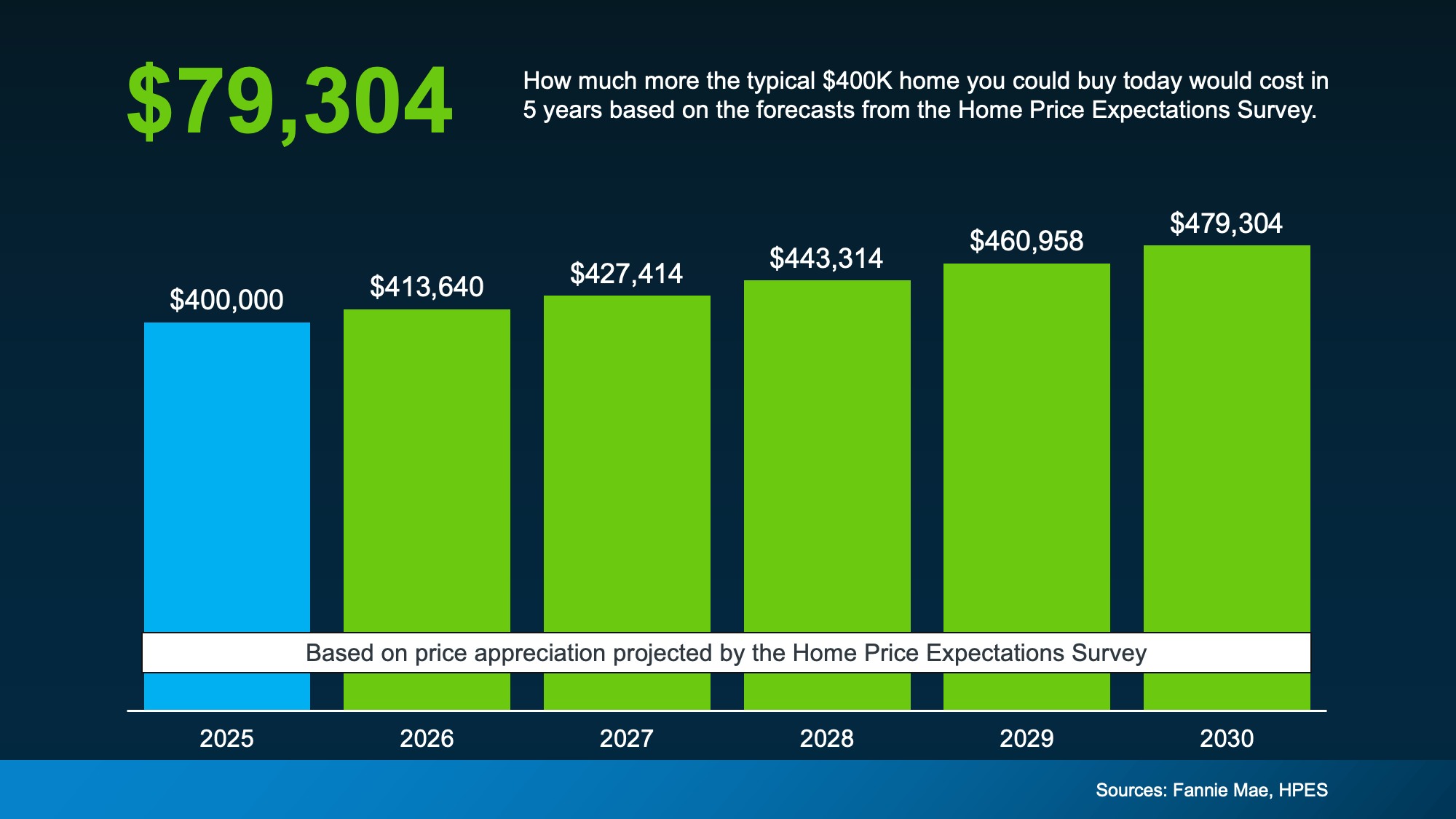

That’s $80K you could be gaining in home value — or losing out on if you keep sitting on the sidelines.

That’s $80K you could be gaining in home value — or losing out on if you keep sitting on the sidelines.

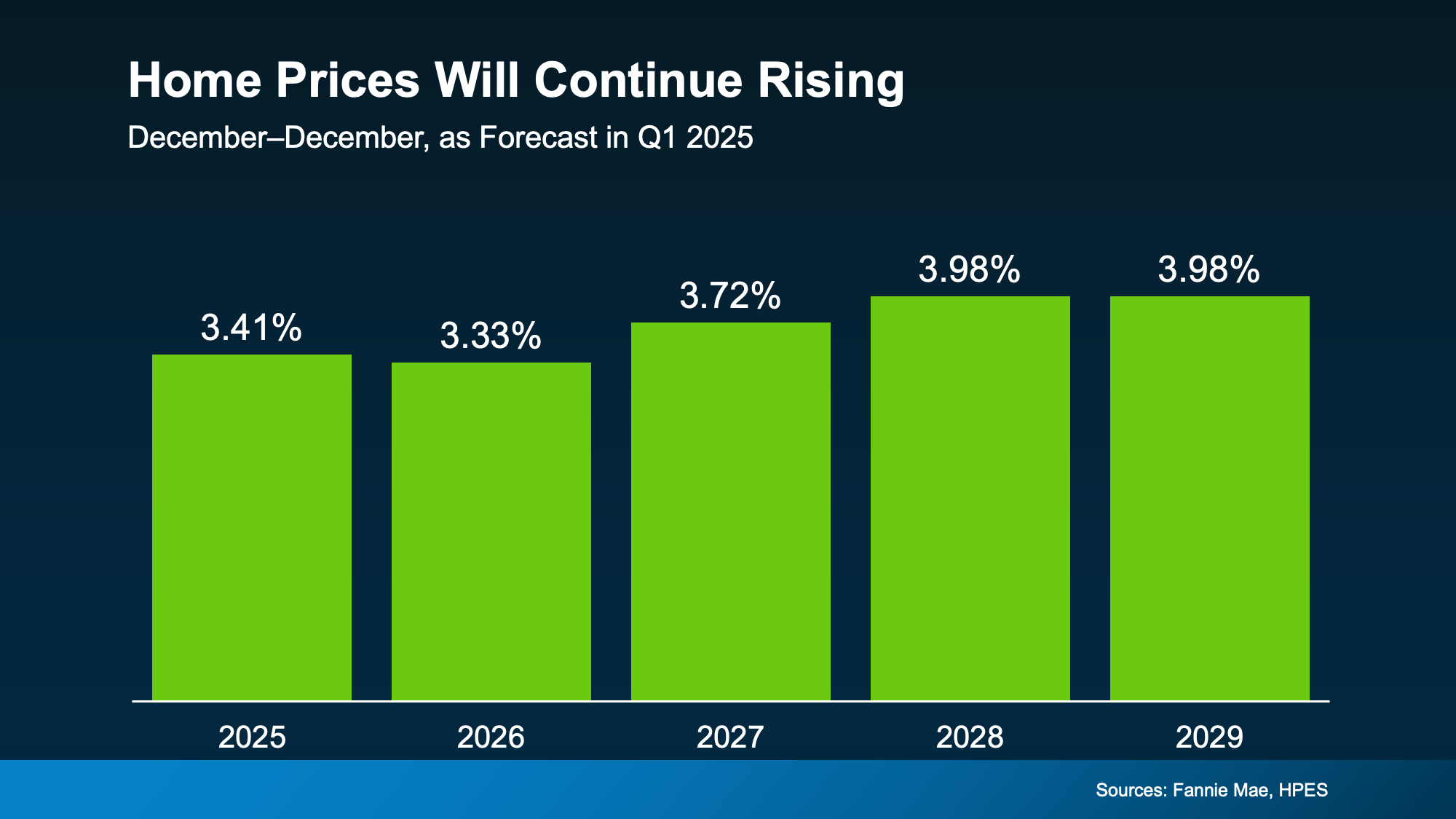

That means the longer you wait, the more your future home will cost you.

That means the longer you wait, the more your future home will cost you.

Follow Us!