Sellers: You’ll Likely Get Multiple Strong Offers This Season

Are you thinking about selling your house right now, but you’re not sure you’ll have the time to do so as the holidays draw near? If so, consider this: even as the holiday season approaches, there are plenty of buyers out there, and they really want your house. Here’s why selling this winter is a win for you.

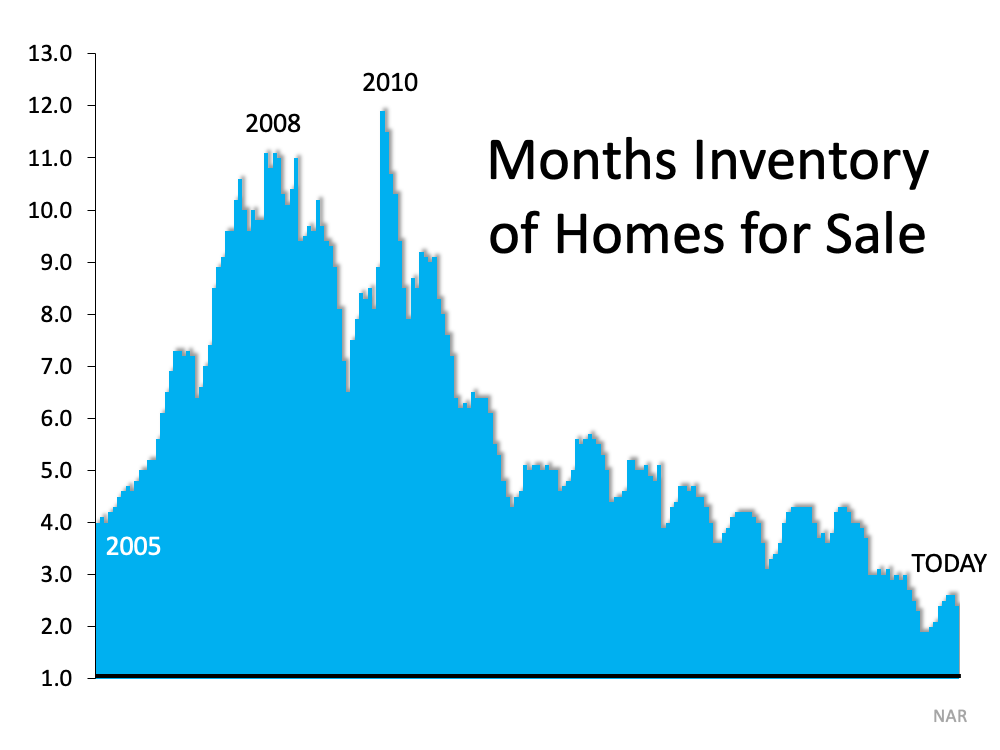

Today’s buyers are still dealing with a limited number of homes for sale. Thanks to continued low inventory, those buyers are competing with one another for their dream home. And when that happens, if your house is one of the few on the market, it will rise to the top of the pool – and it will be worth it.

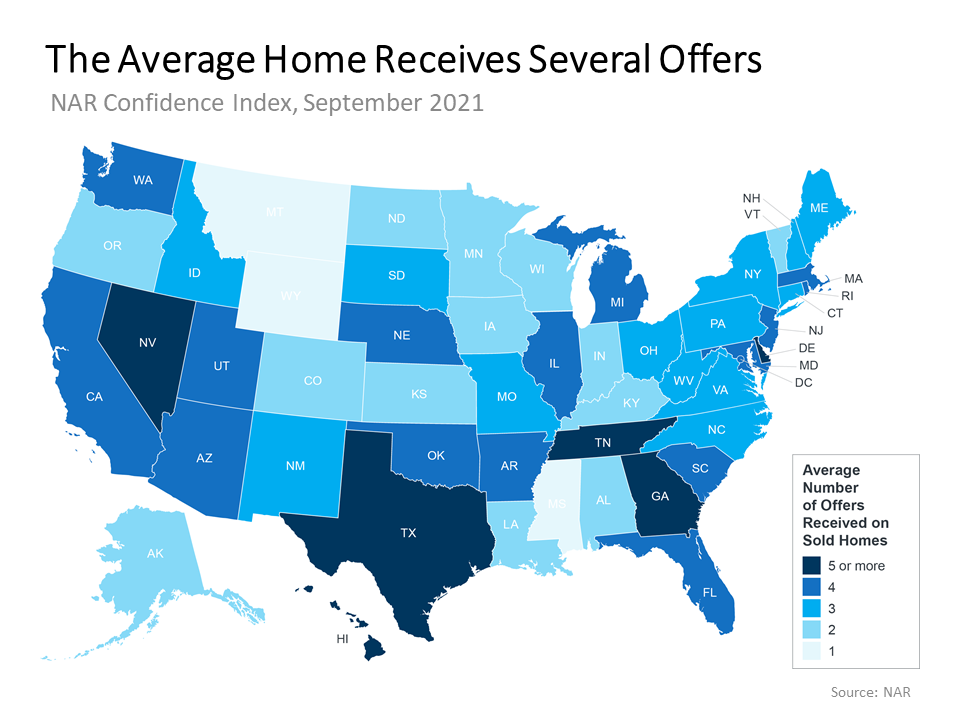

According to the latest data from the National Association of Realtors (NAR), the average seller received 3.7 offers on their house in September. For a view into what’s happening at the state level, take a look at the map below: Nationwide, the average seller today is getting nearly four offers. That number is significant because it means you’ll likely have multiple offers to pick from if you sell your house this season. To put things into perspective, no matter where your state falls, remember that you really only need one good offer to close the deal.

Nationwide, the average seller today is getting nearly four offers. That number is significant because it means you’ll likely have multiple offers to pick from if you sell your house this season. To put things into perspective, no matter where your state falls, remember that you really only need one good offer to close the deal.

Any offer you receive will likely be from a highly motivated buyer who’s doing everything they can to beat the competition. The stakes for buyers are high. They’ve been looking for a house and they want to lock in their dream home before prices and mortgage rates rise further next year. Chances are, they’ll get creative with the terms of their offer, which could include waiving contingencies and offering over the asking price – both of which are great news for you.

If you’re on the fence about when to sell, remember your house is a hot commodity this season. As other sellers take a break for the holidays with plans to re-list their homes in the new year, you can put your house in front of motivated buyers by making your move today. That means your house will be the center of attention, and likely the center of a bidding war too.

Bottom Line

Selling now gives you even more opportunity to win big as buyers compete for your house in today’s market.

![Should I Update My House Before I Sell It? [INFOGRAPHIC] | Simplifying The Market](https://denverlivinghomes.com/wp-content/uploads/2021/11/20211112-KCM-Share-549x300-1.png)

![Should I Update My House Before I Sell It? [INFOGRAPHIC] | Simplifying The Market](https://denverlivinghomes.com/wp-content/uploads/2021/11/20211112-MEM.png)

![Numbers Don’t Lie – It’s Still a Great Time To Sell [INFOGRAPHIC] | Simplifying The Market](https://denverlivinghomes.com/wp-content/uploads/2021/11/20211105-KCM-Share-549x300-1.png)

![Numbers Don’t Lie – It’s Still a Great Time To Sell [INFOGRAPHIC] | Simplifying The Market](https://denverlivinghomes.com/wp-content/uploads/2021/11/20211105-MEM.png)

Follow Us!